The Best Time to Invest

Since the stock market at times can seem a bit like a rollercoaster I am often asked if “now” is a good time to invest. My answer is: it’s always a good time if you are investing for the long term (>5 years). It’s a lot like the old Chinese proverb - “The best time to plant a tree was 20 years ago. The second best time is now.”

If the history of the stock market is our guide, in twenty years you will be really glad if you decided to invest today and will likely wish you had invested more. Despite this fact, many are still hesitant to invest because they fear that the moment they do the stock market will drop. No one wants to buy “high” only to see their investments go lower. I can’t say I blame them, but the only trouble is that it is impossible to predict what the market will do over the next few weeks or months. However, there is a strategy to help those who might be hesitant to invest to start doing so.

Say Hello to My Little Friend called Dollar Cost Averaging

What exactly is this Dollar Cost Averaging (DCA)? DCA is a strategy in which you invest in the stock market at regular intervals (weekly, monthly etc.). Many already employ such a strategy through contributions to their retirement accounts (401k’s, IRA’s etc.). With DCA you are investing regardless of whether the stock market is “high” or “low”. If the market is lower, you are buying; if the market is up, you are still buying. The benefit of the strategy is that it helps remove the emotion from investing.

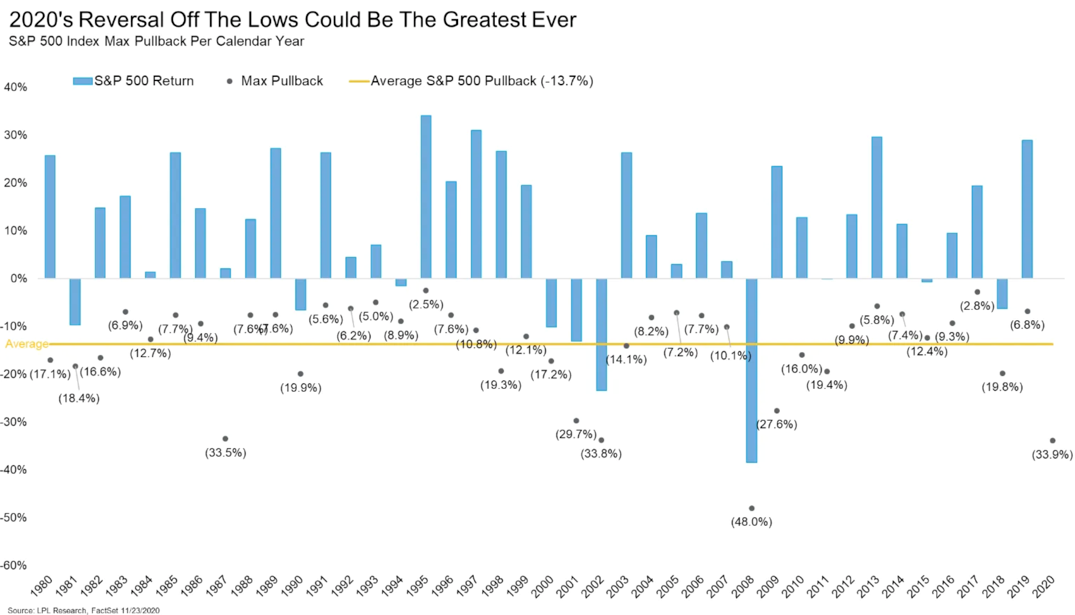

Why You Might Benefit from Dollar Cost Averaging

Take a look at the graph below from LPL financial that shows, with a black dot, the lowest point (max pullback) at which the stock market was down during the year, and the blue bar that shows where the market ended up on December 31st for each respective year (calendar year). As you can see, since 1980 it’s always higher at the end of the year than its lowest point during the year. Therefore, if you are periodically investing you may have benefited from those intra-year downturns by buying more stock at lower prices. It’s also interesting to note that on average the stock market is down -13.7% every year, and yet returns ended up positive for 30 of the last 40 years.

What If You Have a Larger Sum of Money to Invest? Is DCA the Best Strategy?

Great question, but you may be surprised by the answer! According to research around 66%* of the time you would earn a higher return by investing the entire amount all at once (lump sum) than if you followed the dollar-cost averaging approach and spread the investments over the course of 12 months instead. The reason is fairly simple. The market generally moves higher, and by investing a lump sum more of your money would increase when the market moves higher.

When DCA Should Be Considered for Lump Sums

Although you would be up more around 66% of the time if you invested the lump sum versus DCA over a year, some worry a lot about the 34% of the time when you would have less. This certainly makes sense considering the principle of loss aversion. People far prefer avoiding losses to acquiring equivalent gains. Some studies have suggested that losses are twice as powerful, psychologically, as gains*.

So what’s a person to do? Since the most important aspect of building wealth is being invested, DCA can provide many with the confidence to invest. For many clients the strategy I recommend is investing 50% of the lump sum and DCAing the remainder over a 6-9 month period.

My Own Analysis

I was intrigued by the fact that there are downturns of short duration almost every year and wanted to see when these occurred. Consequently, I downloaded the daily close of the S&P500 for the last 40 years, that’s over 10,000 trading days, and determined the following:

The Last 40 years

• There was a total of 21 times where the market low was during the first 3 months of the year, and the market high that same year was in the last 3 months of the year.

• Of those 21 times there were 11 different years the low occurred in January, and the high that same year occurred in December.

• There were also 4 other years when the market high for the year occurred in January.

What can one learn from this unscientific analysis about when to invest? Nothing more than what we already know which is that the ups and downs of the market are not dictated by the calendar but are random. It also shows your best bet is to invest throughout each year and stay invested.

Back to the Future

One of the more interesting things I discovered with my analysis was from the most recent Covid correction. The market low this year occurred on March 23rd when the S&P500 closed at 2237.39. The last time the S&P500 was that low was in November/December 2016! Investors dream about the ability to go back in time and purchase stocks at lower prices, but those that were investing regularly throughout the year did just that when they invested back in March.

The Case for Regular Rebalancing

As just mentioned, the stock market hit a low on March 23 this year. For many of my clients we rebalance investments on a quarterly basis. Meaning at the end of March, June, September, and December we re-adjust the ratio of stocks to bonds. For example, if they were invested in a 60% stock and 40% bond portfolio, 60% of their investments should be in stocks and 40% in bonds. However, at the end of March of this year because of the downturn, the percentage of their stocks would have dropped below 60% and consequently the accounts are rebalanced, meaning bonds were sold and stocks were purchased (at these lower prices) to get back to the 60/40 ratio. While it’s true we benefited that the market downturn occurred near the end of the quarter, it doesn’t lessen the positive impact it had when the portfolios were rebalanced.

Just Set It and Forget It

Dollar Cost Averaging is a simple habit that can build wealth over the long term. Unfortunately, many don’t apply this principle as we get many requests at tax filing deadlines to make an entire years’ worth of contributions. I’ve been guilty of it myself but have since repented.

Why Not Just Time the Downturns Instead?

Now some might look at the chart above and figure they could wait until the downturn occurred and invest then. Unfortunately that’s just not realistic unless of course you can predict the future, which makes me wonder why you would be reading this blog in the first place.

For the record, two of the greatest investors in the world: namely Warren Buffet and the late John Bogle (founder of Vanguard), have both said that they have never met anyone that could time the market. As the saying in the industry goes, “it’s not timing the market but rather time in the market that makes wealth.”

In Conclusion

If you are investing for the long term, it’s always a great time to get into the market, and Dollar Cost Averaging can be a way to help those that may worry about investing a lump sum ease into it.

Thanks for taking the time to read and should you have any questions, feel free to reach out. For those that don’t invest with me, feel free to schedule a free second opinion review of your investments and strategy.

Resources:

*https://www.deseret.com/1997/6/29/19320793/lump-sum-pays-more-than-gradual-investment

*https://investor.vanguard.com/investing/online-trading/invest-lump-sum

*Kahneman, D. & Tversky, A. (1992). "Advances in prospect theory: Cumulative representation of uncertainty". Journal of Risk and Uncertainty. 5 (4): 297–323.